RV Financing Canada: Fast Approval for All Credit Types

Whether you’re eyeing a Class A motorhome parked on a dealer lot in Calgary or a used fifth wheel listed privately in Muskoka, financing your RV through the right lender network makes all the difference. Finance That connects Canadian buyers with 30+ specialized lenders, so you get competitive rates and real approval — not just a pre-qualification that evaporates at the dealership.

Whether you’re purchasing personally or for your business, Finance That makes it easy to apply and get approved with flexible financing options tailored to your needs.

Competitive rates starting from 6.99%*

Buy from a dealer or private seller

Personal & commercial financing options

Fast approvals with no obligation

*Rates vary based on credit profile, asset type, and lender approval.

By submitting, you agree to be contacted by Finance That via SMS and email about your application. To provide financing options, we may review your credit profile using a soft check that does not affect your score. You can unsubscribe anytime.

How RV Financing Works at Finance That

Getting an RV loan shouldn’t take longer than a weekend hike. The process runs in three clear steps, and most applicants receive same-day pre-approval.

Apply Online in 2 Minutes

Complete a single application from any device. The initial inquiry uses a soft credit check — zero impact on your credit score. You'll enter basic personal information, income details, and the RV you have in mind. No obligation at this stage.

Get Matched With Your Best Lender

The application routes simultaneously to over 30 Canadian lenders. They compete for your business. A dedicated financing specialist reviews the competing offers and presents the lowest rate and best terms available for your credit profile.

Sign Digitally and Drive Away

Once you accept an offer, documents are issued electronically. Sign from your laptop or phone. Funds are released directly to the dealership or private seller. Transfers typically clear within one to two business days.

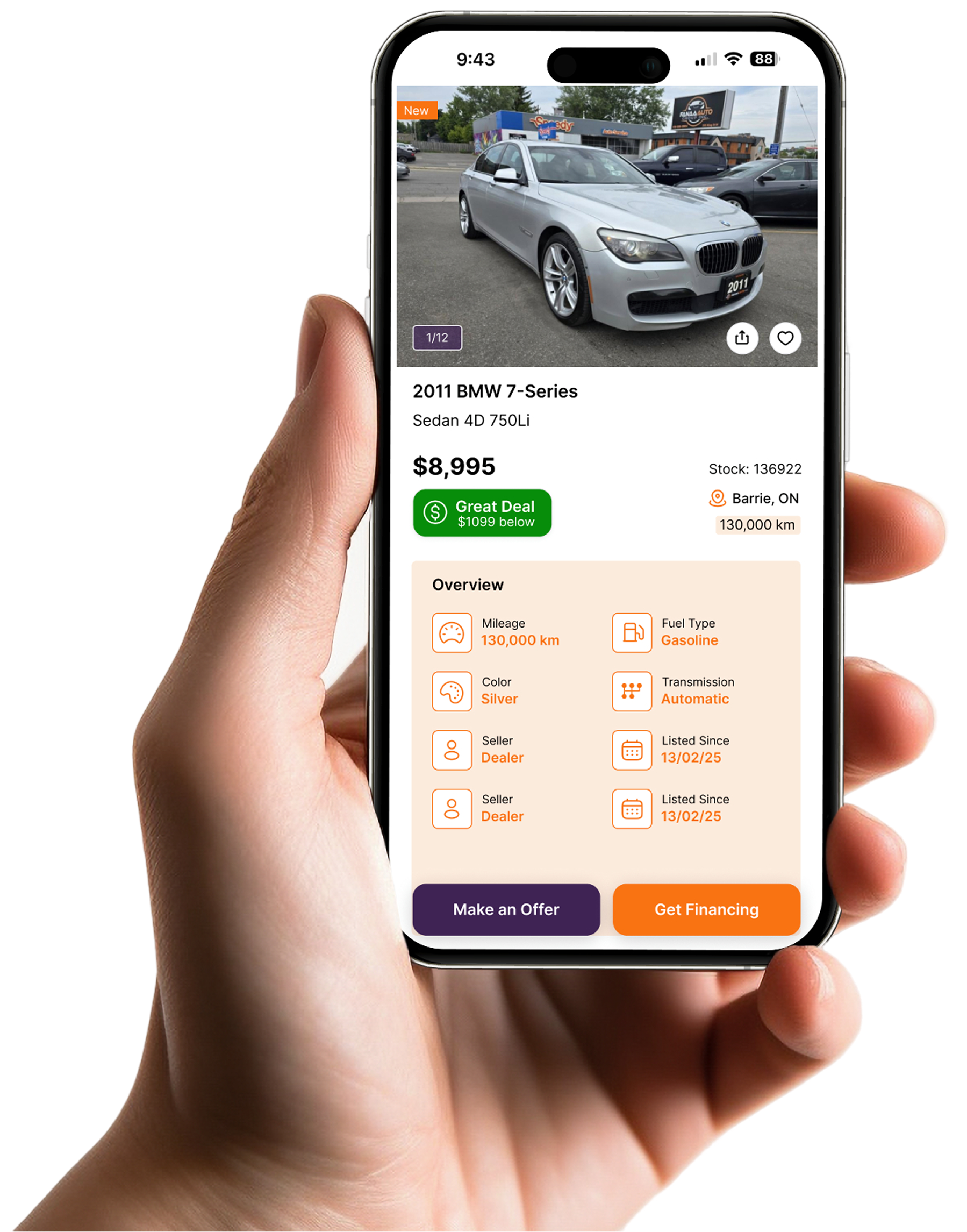

Browse 1000s of Listings

Find What You Need.

Get Approved. Move Forward.

Browse cars, trucks, ATVs, RVs, and commercial equipment, all available with fast, flexible financing through the Finance That Marketplace.

Compare, and apply for financing in minutes, directly from any listing. Whether you’re purchasing personally or for your business, we make it simple to get approved and move forward without the back-and-forth.

There’s no shortage of financing options in Canada. With Finance That, a single application reaches over 30 Canadian lenders simultaneously. Banks, credit unions, and specialty recreational vehicle lenders all compete for your file. You see the best offer, not just the first one.

Also You get a Dedicated Financing Specialist who handles your file from application to funding. They answer questions, negotiate lender conditions, and coordinate document collection.

The best deal on your next RV might be listed on Kijiji or Facebook Marketplace rather than at a dealership. Finance That facilitates private sale RV financing — a process that requires a few extra steps but is entirely manageable.

Step 01

Find your RV

Identify the private seller, agree on a price, and confirm the VIN.

Step 02

Apply for financing

Submit the standard 2-minute application and include the vehicle details (year, make, model, VIN, asking price).

Step 03

Lien check completed

Finance That orders an PPSA (Personal Property Security Act) lien search on the VIN to confirm the seller has clear title and no outstanding loans registered.

Step 04

Inspection arranged

Most lenders require a third-party inspection for private sale RVs. Finance That coordinates this through a network of inspection services across Canada. Cost: typically $150–$300.

Step 05

Funds released to seller

Once the lender approves, funds are sent directly to the seller via bank draft or electronic transfer. The seller doesn't receive cash from you the lender pays them directly.

Step 06

Title transferred

Ownership documents are transferred to you, and you begin repayment.

For a complete walkthrough, read the blog post on private sale RV financing in Canada.

Frequently Asked Questions

What credit score do I need for RV financing in Canada?

There is no hard minimum credit score. Finance That has lenders who approve applications with scores below 500, though rates are higher and a down payment is typically required below 550. Applicants with scores above 700 qualify for the best available rates, starting at 7.99%.

How long can I finance an RV for?

RV loan terms in Canada run from 1 to 20 years through Finance That’s network. Longer terms are available on newer, higher-value RVs. Older RVs (15+ years) may be capped at 10–12 year terms depending on the lender.

Can I finance a used RV?

Yes. Finance That finances both new and used RVs. Most lenders in the network accept used RVs up to 15–20 years old. RVs older than 15 years may face higher rates or require a larger down payment.

Do I need a down payment for an RV loan?

Not necessarily. Prime and near-prime borrowers frequently receive $0 down approval. Subprime and deep subprime applicants typically need 10–20% down to secure approval. A larger down payment always improves the rate offered regardless of credit tier.

Can I finance a private sale RV?

Yes. Finance That specializes in private sale RV financing. The process includes a PPSA lien search, third-party inspection, and direct payment to the seller. Full details are covered in the Private Sale section above and in the blog post on private sale RV financing.

Is RV insurance required for financing?

Yes. All lenders in Finance That’s network require proof of insurance before releasing funds. RV insurance must list the lender as loss payee. If you don’t have a provider, Finance That can connect you with recreational vehicle insurance specialists at no referral cost.

Will applying for RV financing affect my credit score?

The initial inquiry uses a soft credit check — no impact on your score. A hard credit pull only occurs when you authorize a full credit application with a specific lender. Finance That will always ask for your permission before initiating a hard pull.

Can I pay off my RV loan early?

This depends on the lender. Some lenders charge a prepayment penalty — typically 3 months’ interest — while others allow full or partial prepayment at any time with no penalty. Your financing specialist will confirm the prepayment terms before you sign.

How quickly can I get approved?

Most applicants receive a pre-approval decision the same day. Full approval with funding typically takes 1–3 business days once all documents are submitted. Private sale financing takes slightly longer (3–5 business days) due to the lien search and inspection requirements.

What's the difference between financing through Finance That versus a bank?

Applying directly at a single bank means your application is evaluated against that one institution’s criteria and rate card. Finance That submits your application to 30+ lenders simultaneously, generating competing offers. This typically results in a lower rate, more flexible terms, and a significantly higher approval probability.

Ready to Finance Your RV? Get Approved in 24 Hours.

Thousands of Canadians have financed their RV through Finance That’s lender network from first-time buyers working through a consumer proposal to prime borrowers picking up a $180,000 Class A motorhome. The application takes two minutes, the soft credit check costs you nothing, and a specialist is standing by to match you with the best available offer.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.